The graphene industry is advancing beyond the laboratory stage, with robust growth projected.

Graphene has long been hailed as a wonder material, but its commercial journey has been defined by cautious progress rather than overnight disruption. Today, the industry is steadily advancing beyond the laboratory stage. IDTechEx projects robust growth for graphene-related materials in the coming decade, driven by expanding demand across multiple application sectors.

For more than a decade, IDTechEx has been at the forefront of tracking the evolution of graphene and other nanomaterials. Since launching its first dedicated reports on carbon nanotubes (CNTs) in 2011 and graphene in 2012, the organization has conducted hundreds of interviews across the global value chain. This extensive research provides an unparalleled view of technological advancements, commercialization efforts, and the long-term market potential of these materials.

IDTechEx does not focus solely on material suppliers but also covers the end-use industries where these materials must ultimately compete. IDTechEx has released a new report, "Graphene & 2D Materials 2026-2036: Technologies, Markets, Players", which includes granular 10-year graphene market forecasts, based on profiles of 90+ key players and leverages extensive in-depth coverage of many end-use markets for graphene.

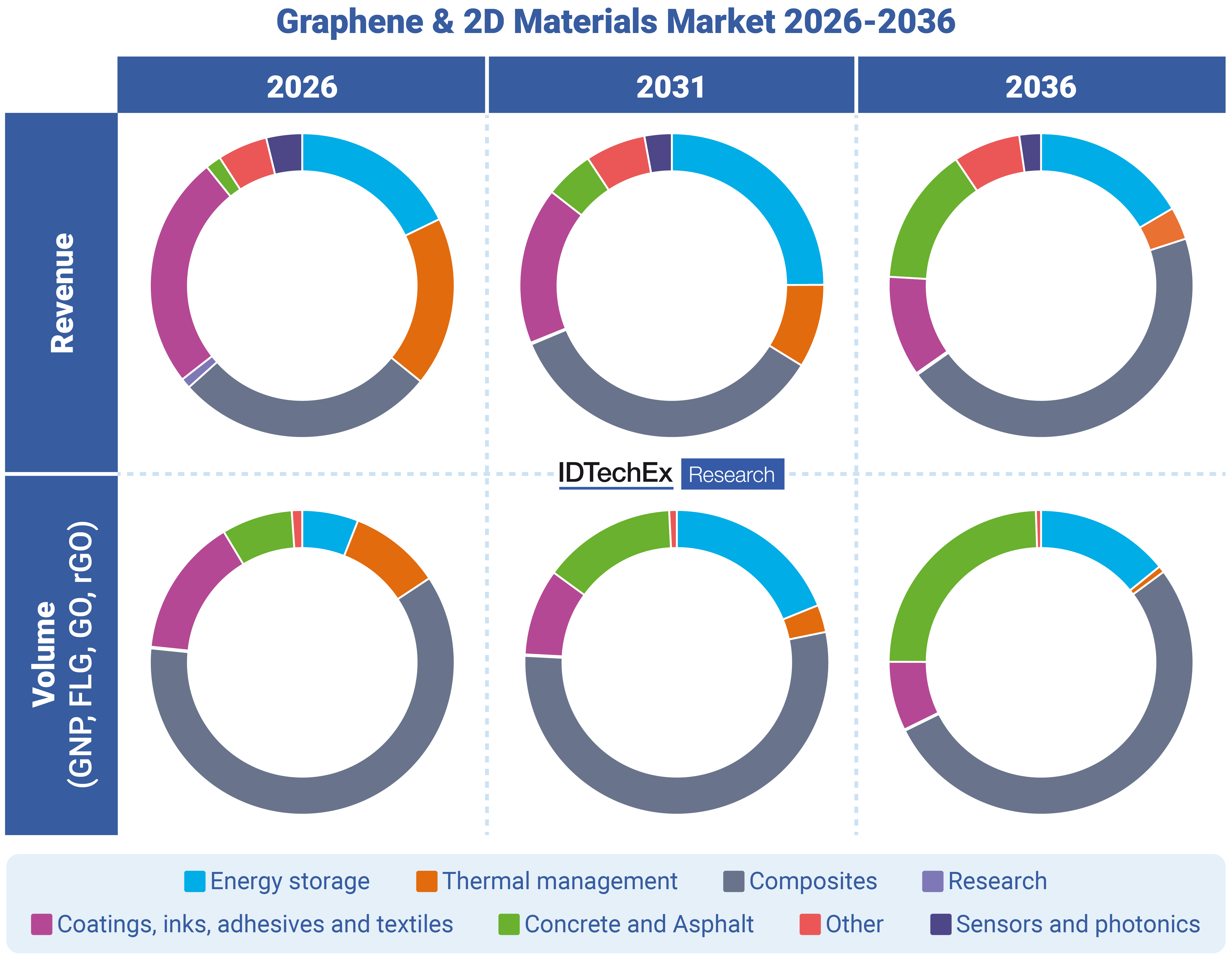

Graphene is not a single product but a family of materials, including graphene nanoplatelets (GNP), graphene oxide (GO), and reduced graphene oxide (rGO). Each has different structural properties and commercial prospects, and while standardization efforts are underway, regulatory and safety challenges remain. Benchmarking studies in the report show that GNPs, GO, and rGO are leading the charge toward large-scale adoption.

Signs of accelerated market uptake are increasingly visible. Automotive companies are testing and adopting graphene-enhanced composites, smartphone makers are deploying graphene in heat spreaders, and industries are turning to it for elastomers, coatings, and corrosion resistance. The value lies not in a "one-size-fits-all" material, but in the ability to optimize morphology, purity, and dispersion for each specific application. Companies are now competing to control this crucial intermediate step in the value chain, either internally or through strategic partnerships.

Manufacturing, Consolidation, and the Path Forward

Graphene production methods remain diverse. Top-down approaches such as liquid-phase exfoliation and oxidation-reduction dominate today, but new entrants are experimenting with alternative feedstocks and more efficient processes. The market, however, is crowded. Hundreds of manufacturers currently operate worldwide, but history suggests consolidation is inevitable as a few strong players emerge. Early signs of this trend are already visible.

China has quickly become a leader in both production capacity and academic research, shaping the global competitive landscape. Still, despite rising revenues across the sector, profitability remains elusive. Only a handful of companies have reached sustained positive margins, with many still dependent on public and private funding. This underscores the difficulty of transitioning from "material push" to "market pull", which is a challenge common to many advanced technologies.

Image source: Graphene & 2D Materials 2026-2036: Technologies, Markets, Players - IDTechEx

Where Will Graphene Find Its Strongest Foothold?

The applications for graphene are vast, but the most promising sectors today include composites, energy storage, thermal management, coatings, concrete, and textiles. Each sector presents unique drivers: lightweighting for automotive, improved product lifetimes for industrial uses, or sustainability considerations in construction. The report provides detailed ten-year projections for revenue and volumes across 18 distinct end-use applications, offering a roadmap for companies and investors alike.

Graphene films and wafers, produced primarily via chemical vapor deposition (CVD), represent another avenue of growth. Initially targeted for transistors and transparent conductive films, these applications faced setbacks due to material limitations and competition from established alternatives. However, commercial success is now emerging in areas such as sensors and optoelectronics, where graphene's unique properties deliver clear performance advantages. With ongoing improvements in manufacturing, these markets are expected to expand significantly over the next decade.

Learning from Other Nanocarbons

Graphene's trajectory can also be better understood by examining the history of other advanced carbons. Carbon black, for example, is a well-established conductive additive with global scale and low margins. Its entrenched role highlights the hurdles GNPs and rGO must overcome to achieve large-scale market penetration. Similarly, carbon nanotubes provide valuable lessons. Multi-walled CNTs expanded too aggressively before applications materialized, only finding strong demand in recent years in lithium-ion battery cathodes. Single-walled CNTs, meanwhile, continue to hold promise but lack a dominant commercial use case. These precedents suggest that patience and careful targeting of niche applications are essential for graphene's success.

For more details on the graphene market, including a segmentation by application area, see the IDTechEx market report "Graphene & 2D Materials 2026-2036: Technologies, Markets, Players". For more information on IDTechEx's other reports and market intelligence offerings, please visit www.IDTechEx.com/Research.

IDTechEx guides your strategic business decisions through its Research, Subscription and Consultancy products, helping you profit from emerging technologies. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.